The Bourse ended the week on a negative note as the ASPI decreased by 23.82 points (or -0.37%) to close at 6,331.10 points, while the S&P SL20 Index also decreased by 13.00 points (or -0.37%) to close at 3,526.93 points.

Turnover and market capitalization

Commercial Bank was the highest contributor to the week’s turnover value, contributing LKR0.52Bn or 25.86% of total turnover value.

Hemas Holdings followed suit, accounting for 19.84% of turnover (value of LKR0.40Bn) while HNB contributed LKR0.08Bn to account for 4.13% of the week’s turnover.

Total turnover value amounted to LKR2.00Bn (cf. last week’s value of LKR2.83Bn), while daily average turnover value amounted to LKR0.50Bn (-11.64% W-o-W) compared to last week’s average of LKR 0.57Bn.

Market capitalization meanwhile, decreased by 0.37% W-o-W (or LKR 11.06Bn) to LKR 2,956.65Bn cf. LKR 2,967.70Bn last week.

Liquidity (in value terms)

The Banking, Finance & Insurance sector was the highest contributor to the week’s total turnover value, accounting for 47.26% (or LKR 0.95Bn) of market turnover.

Sector turnover was driven primarily by Commercial Bank, HNB, Sampath Bank and Sanasa Development Bank which accounted for 75.71% of the sector’s total turnover.

The Diversified sector meanwhile accounted for 29.15% (or LKR 0.58Bn) of the total turnover value, with turnover driven primarily by Hemas Holdings, Melstacorp and JKH which accounted for 88.56% of the sector turnover.

The Beverage, Food & Tobacco sector was also amongst the top sectorial contributors, contributing 9.19% (or LKR 0.18Bn) to the market driven by Renuka Agri Foods and Ceylon Tobacco which accounted for 62.35% of the sector turnover.

Liquidity (in volume terms)

The Beverage, Food & Tobacco sector dominated the market in terms of share volume, accounting for 41.83% (or 36.71Mn shares) of total volume, with a value contribution of LKR 0.18Bn. The Banking, Finance & Insurance sector followed suit, adding 17.75% to total turnover volume as 15.58Mn shares were exchanged.

The sector’s volume accounted for LKR0.95Bn of total market turnover value.

The Diversified sector meanwhile, contributed 12.26Mn shares (or 13.97%), amounting to LKR0.58Bn.

Top gainers and losers

Swarnamahal Finanace and Adam Capital were the week’s highest price gainers; Swarnamahal Finance increased by 20.0% W-o-W from LKR1.50 to LKR1.80.

Swarnamahal Finanace and Adam Capital were the week’s highest price gainers; Swarnamahal Finance increased by 20.0% W-o-W from LKR1.50 to LKR1.80.

Adam Capital gained 20.0% W-o-W to close at LKR0.60. Tess Agro [NV] (+16.7% W-o-W) and Royal Palms (+14.8% W-o-W) were also amongst the top gainers.

SMB Leasing [NV] was the week’s highest price loser, declining 33.3% W-o-W from LKR0.30 to LKR0.20. Blue Diamonds’ Voting (-25.0% W-o-W) & Non-Voting shares (-12.5% W-o-W) and Ramboda Falls (-13.5% W-o-W) were also amongst the top losers over the week.

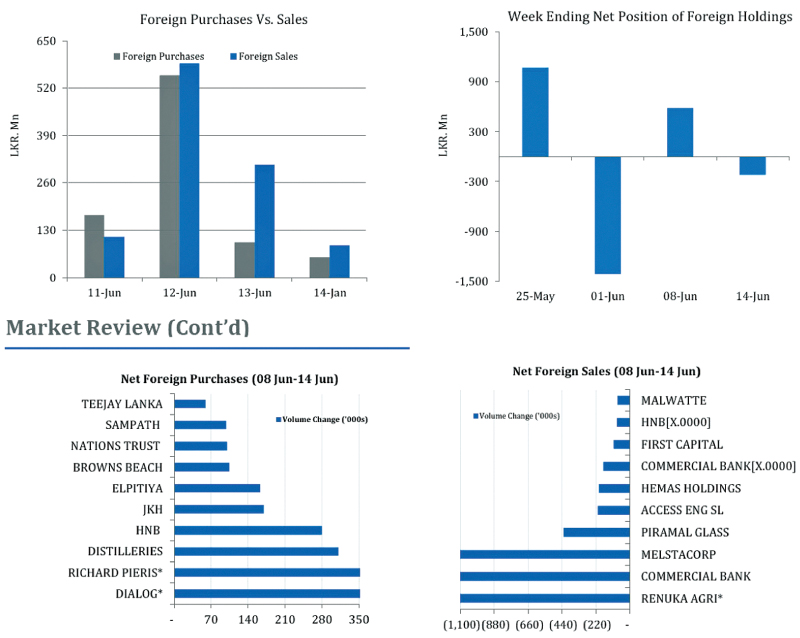

Foreign investors closed the week in a net selling position with total net outflow amounting to LKR 0.22Bn relative to last week’s total net inflow of LKR 0.59Bn (-137.3% W-o-W).

Total foreign purchases decreased by 35.5% W-o-W to LKR 0.88Bn from last week’s value of LKR 1.37Bn, while total foreign sales amounted to LKR 1.10Bn relative to LKR 0.78Bn recorded last week (41.36% W-o-W).

In terms of volume Dialog & Richard Pieris led foreign purchases while Renuka Agri & Commercial Bank led foreign sales.

In terms of value HNB & Dialog led foreign purchases while Commercial Bank & Renuka Agri led foreign sales.

Point of view

Sri Lankan Equities continued to dip for the 4th consecutive week as the benchmark ASPI lost ~24 points (0.37% W-o-W) to close the week at a YTD low of 6,331.10. Continued losses in local equities were mainly driven by lower activity levels as most major categories of investors remained on the sidelines. Activity levels on the bourse hit a 9-week low as the turnover declined ~29% W-o-W to Rs.2.0Bn (cf. Rs.2.8Bn last week) while daily average turnover for the week declined to a 6-week low of Rs.0.5Bn (cf. Rs.0.6Bn last week).

The low activity levels were primarily due to poor participation levels by Local Institutional and HNI investors who remained on the sidelines this week.

Crossings for the week accounted for just ~17% of the week’s turnover with Commercial Bank accounting for ~27% of the crossings.

Negative investor sentiment has continued to drag domestic equities since May’18, resulting in the ASPI dropping ~3.1% between May-June to convert the positive return on the ASPI (up to April) down to a negative -0.6% YTD.

The YTD loss on the more liquid S&P20 Index meanwhile, widened further during the week to 3.9% indicating the persistent negative investor sentiment.

Foreign investor flows to the Bourse meanwhile turned negative this week, despite a net inflow of Rs.60Mn on Monday.

Net foreign outflows over the week consequently totaled Rs.219Mn (cf. inflow of Rs.588Mn last week), reducing the net foreign inflows to CSE so far in Jun’18 down to Rs.603Mn. Despite this week’s foreign equity sell-off though, so far in Q2’18, foreign appetite for Sri Lankan equities has remained positive with total net inflows in Q2’18 totaling ~Rs1.7Bn (cf. outflow of Rs.2.6Bn in Q1’18).

Markets in the week ahead are likely to look for cues from further economic and political developments.

March 2018 quarter earnings rise 25% Y-o-Y

Total market earnings for the recently concluded earnings season indicated Y-o-Y growth, with earnings2 for the Mar’18 quarter rising 25% to Rs.99.3Bn.

This compares to the Rs. 79.3Bn recorded by the full market a year ago in Mar’17 and the Rs. 85.4Bn recorded last quarter (in Dec’17).

Growth over the quarter was driven largely by sectors such as Banks, Finance & Insurance, (+31% Y-o-Y), F&B (+71% Y-o-Y), Teleco (+34% Y-o-Y), Diversified (+32% Y-o-Y) and Construction (+60% Y-o-Y).

While the growth over the quarter was notable, it is also largely reflected i) the traditionally stronger March quarter which remains the financial year end for most companies and ii) exceptional gains from several Insurance companies. Stronger Mar’18 quarter earnings also boosted the overall market’s full year earnings, and overall corporate earnings for the FY’17/183 rose 7% Y-o-Y to Rs. 284Bn (cf. Rs. 265Bn last year).

Despite the Y-o-Y growth, the pace of growth was slower at 7% compared to 26% Y-o-Y growth last year, largely reflecting the general slowdown in overall GDP growth which fell to 3.1% Y-o-Y in 2017 (cf. 4.5% Y-o-Y in 2016).

On a trailing 12M basis meanwhile, Sri Lanka’s corporate earnings growth rose 12% Y-o-Y to Rs. 299.8Bn. Growth was driven by the largest three contributors to market earnings, Banks, Finance & Insurance (+28% Y-o-Y), Diversified (+20% Y-o-Y) and F&B (+22% Y-o-Y).

The improvement in market earnings helped maintain the CSE’s current low PER level of 10.09x, the lowest among its Frontier and Emerging market peers which currently trade at 13x (MSCI FM Index) and 14x (MSCI EM Index).

Add new comment